This mental tendency echoes the words of the song: “When I’m not near the girl I love, I love the girl I’m near.” Man’s imperfect, limited-capacity brain easily drifts into working with what’s easily available to it.

— Charlie Munger, Poor Charlie’s Almanack

This is not the article that I planned to publish today. Early last week, I came up with an idea for a timely article that I would post after the end of the second quarter. Imagine my surprise when I sat down on Saturday morning to download and review supporting data and found that the underlying assumptions for my article were entirely incorrect! I had fallen for one of the more common errors explained by Charlie Munger in his examination of the psychology of human misjudgment.

Berkshire Hathaway’s repurchase policy has long been a topic of interest in the value investing community due to the ever-increasing pile of cash that Warren Buffett has been unable to deploy. Repurchases have been quite minor in recent quarters since the policy was changed last year. During the recent annual meeting, both Warren Buffett and Charlie Munger reaffirmed that Berkshire could indeed make meaningful repurchases at prices judged to be well below intrinsic value. The significant drop in Berkshire shares in the weeks following the annual meeting led me to believe that the prospects for major repurchases had increased and that repurchase activity for Q2 was likely to be higher than in Q1.

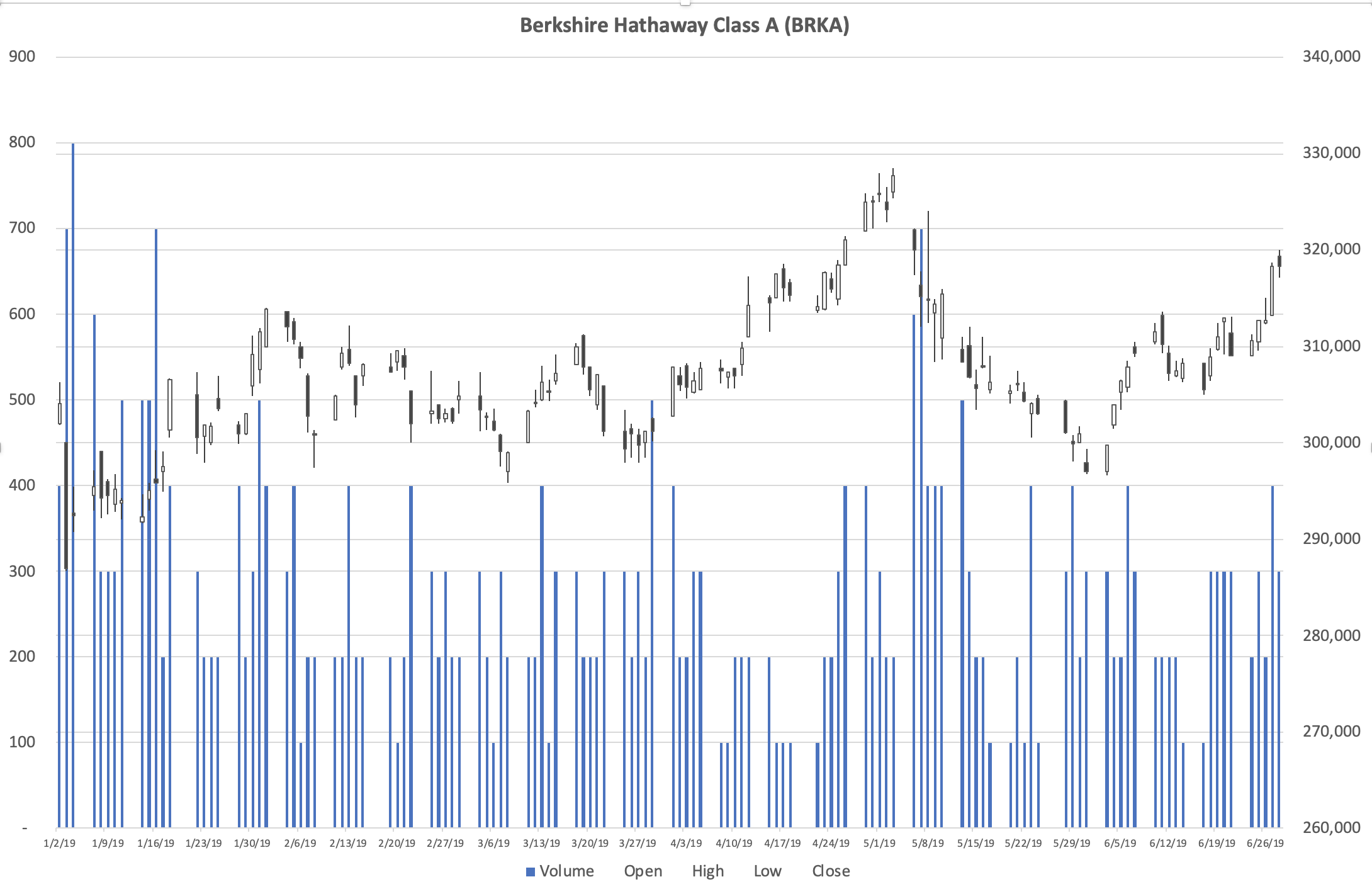

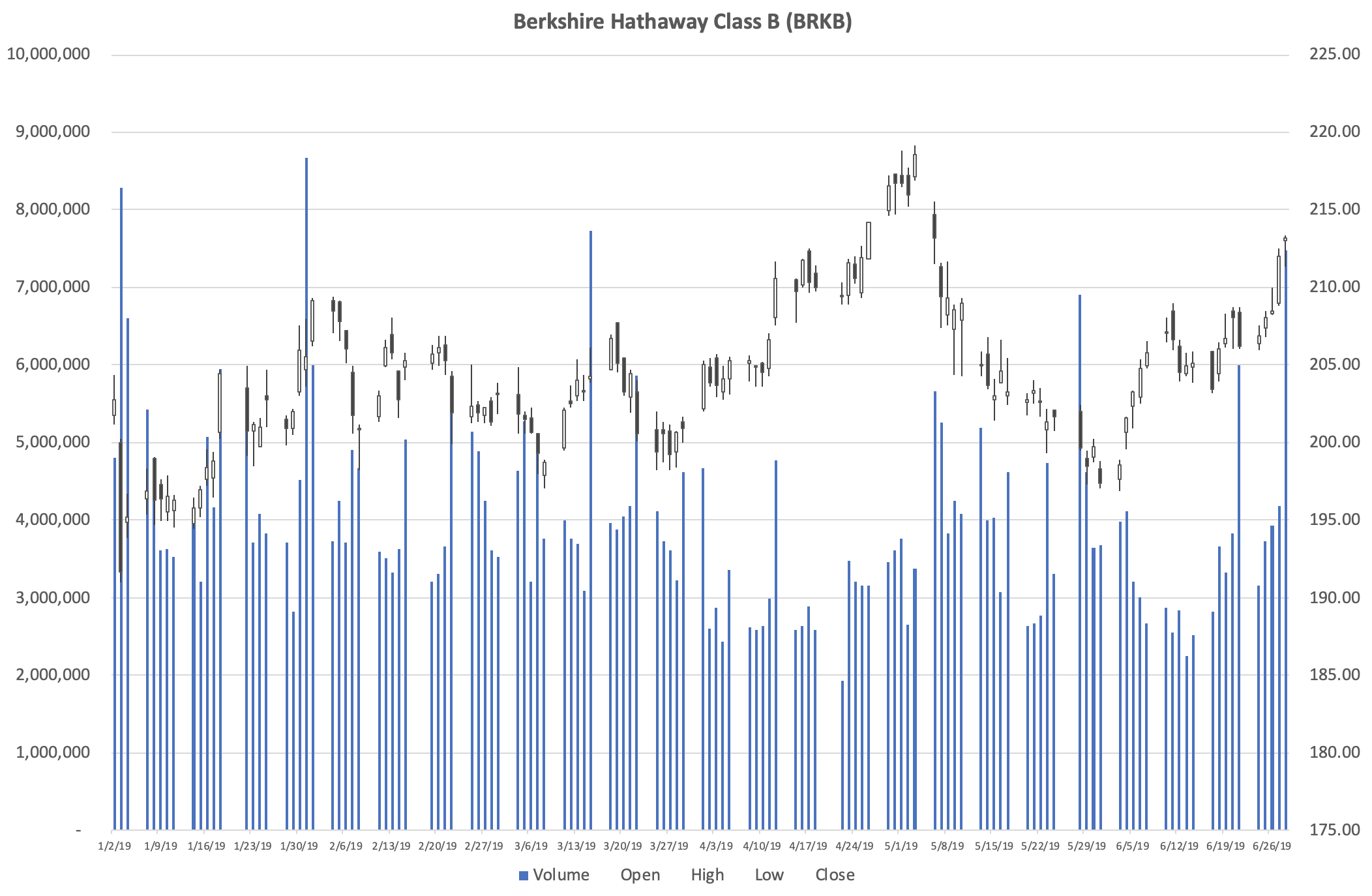

Berkshire’s Class B shares closed at $218.60 on May 3, 2019, the day before the annual meeting, which represented the highest level for the stock since before the December 2018 stock market swoon. Following the meeting, the stock began a month-long decline taking the price down nearly 10 percent by May 31 when it closed at $197.42. The shares subsequently recovered most of the decline during June ending the quarter at $213.17.

Why present a paragraph covering the wiggles in the stock price over the span of a couple of months? Long term owners of businesses should not really care about short term stock price movements or even follow them closely. However, I was watching the price of Berkshire stock during the May stock market decline and the days immediately following the annual meeting were most available in my mind over the past several weeks. This led me to the incorrect assumption that opportunities for repurchase in the second quarter were greater than during the first quarter.

Daniel Kahneman, in his brilliant book, Thinking, Fast and Slow, explains that the ease with which events come to mind heavily influences our cognitive abilities and increases the risk of poor judgment:

The availability heuristic, like other heuristics of judgment, substitutes one question for another: you wish to estimate the size of a category or the frequency of an event, but you report an impression of the ease with which instances come to mind. Substitution of questions inevitably produces systematic errors.

Thinking, Fast and Slow, p. 130

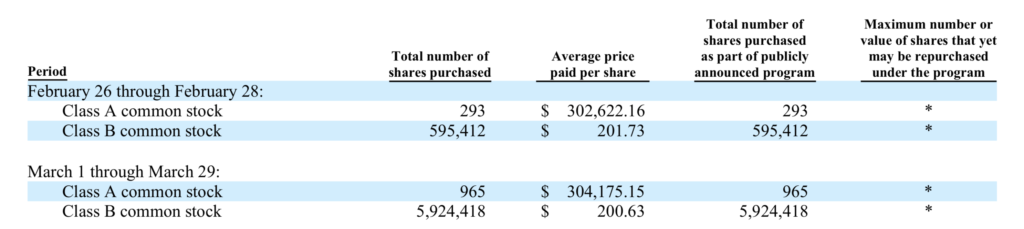

The following exhibit from Berkshire’s first quarter report shows that the company spent $1.69 billion to repurchase Class A and Class B common stock during the quarter:

We can see that repurchases for the quarter commenced on February 26 when shares closed at $201.90 and continued through the last trading day of the quarter on March 29 when shares closed at $200.89. Additionally, Berkshire’s disclosure in the 10-Q of the total share count as of April 25 suggests that modest repurchases continued into April as shares began to rise. The size of the repurchase from April 1 to 25 appears to be approximately 157 Class A share equivalents, and it seems likely that those shares were purchased early in April and that repurchase activity then halted as shares continued to rise.

The following charts (click to enlarge) show trading activity for Berkshire’s Class A and Class B common stock for the first half of 2019:

We can see immediately that the decline in Berkshire shares in May only brought the stock back to levels that were far more common during the first quarter. If we assume that repurchases are probable in significant size under $205 per Class B share, there were 26 trading days between May 1 and June 30 when shares traded below that level at some point during the day. In contrast, there were 56 trading days during the first quarter when shares traded below $205.

We have no way of knowing what Warren Buffett’s current upper limit might be for share repurchases. We can only deduce what he is likely to do based on very recent history, which in this case leads us to look at his pattern of repurchases during the first quarter. It is notable that Berkshire repurchased shares at average prices in excess of $205 during the third and fourth quarters of 2018. Repurchase activity is going to depend on a number of factors including Mr. Buffett’s assessment of the current stock price relative to intrinsic value, which moves upward slowly over time, as well as alternate uses of cash.

The main point of this article isn’t to speculate on the magnitude of repurchases at Berkshire during the second quarter, although that would have been the intent of the original article I had planned to write based on my incorrect “gut feeling” about the May stock price decline. Instead, it serves to remind us that we can be our own worst enemy when it comes to falling victim to cognitive biases, even when we are fully aware of what those biases are and how they have impacted other people. Reading Kahneman and Munger and understanding how these biases work does not confer any sort of immunity on us as human beings. We have to continue to be vigilant to ensure that we are making decisions rationally rather than falling back on lazy heuristics.

It is also worth noting that those who focus too much on current events are at increased risk of falling for the availability-misweighing tendency. The concept of via negativa, or wisdom through subtraction, applies here. Focusing less on current news (and stock market quotations) and more on subjects of enduring value can insulate us against weighing events of the recent past too heavily. Although I refrain from actually updating the quotations in my investment tracking spreadsheets very often, I do follow market activity every day reasoning that my overriding philosophy will prevent me from reacting rashly to short term news. In this case, my misjudgment only resulted in planning to write an article that wasn’t supported by facts. However, the outcome could be much worse if it involved an actual investment decision. I don’t think that I would make a stupid investment decision based on rash judgments precipitated by short terms news. But am I certain? Perhaps a lower information diet shunning day to day market news is in order.

Disclosure: Individuals association with The Rational Walk LLC own shares of Berkshire Hathaway.

Note to readers: This article is part of a series on Charlie Munger’s Psychology of Human Misjudgment.