In Today’s Issue:

This is a special issue of Rational Reflections covering today’s release of Berkshire Hathaway’s 2019 annual report and Warren Buffett’s letter to shareholders.

Topics covered include:

- Berkshire Hathaway’s 2019 Results

- Highlights from Warren Buffett’s Letter to Shareholders

- 2019 Repurchase Activity

- Questions for Ajit Jain and Greg Abel

The next regular newsletter issue will be sent out on Wednesday, February 26.

Berkshire Hathaway 2019 Results

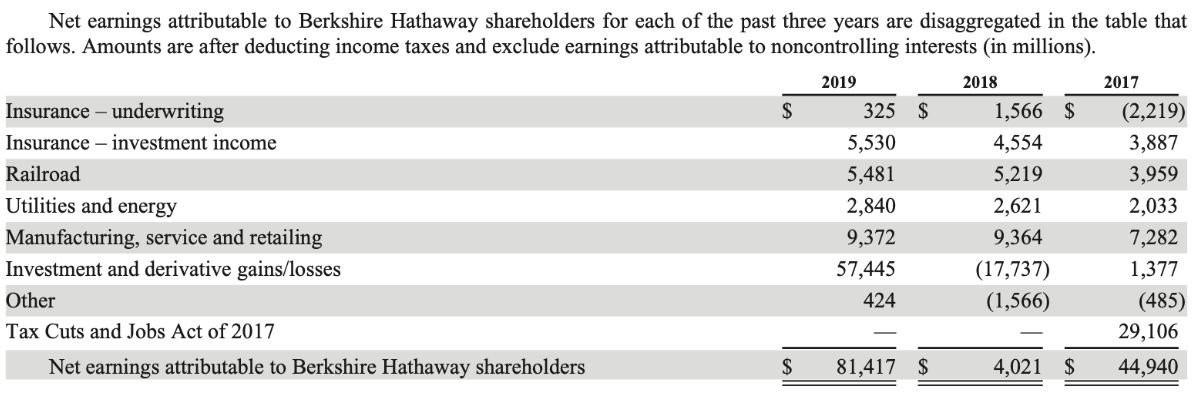

Berkshire Hathaway reported net earnings of $81.4 billion for 2019, up from $4 billion in 2018. However, as both the earnings release and Warren Buffett’s letter to shareholders point out, headline net income for Berkshire can be highly misleading. Accounting changes that took effect in 2018 require Berkshire to include unrealized investment gains and losses in net income. This has created tremendous volatility in reported net income, as Buffett describes in his letter:

“Berkshire’s 2018 and 2019 years glaringly illustrate the argument we have with the new rule. In 2018, a down year for the stock market, our net unrealized gains decreased by $20.6 billion, and we therefore reported GAAP earnings of only $4 billion. In 2019, rising stock prices increased net unrealized gains by the aforementioned $53.7 billion, pushing GAAP earnings to the $81.4 billion reported at the beginning of this letter. Those market gyrations led to a crazy 1,900% increase in GAAP earnings!”

Berkshire’s net operating earnings showed much less excitement, falling from $24.8 billion in 2018 to $24 billion in 2019. Berkshire’s presentation of the components of net income provides a better high level overview of the sources of earnings for the past three years:

The following bullet points provide a very abbreviated 30,000 foot summary view of the drivers of Berkshire’s operating income based on my review of the report earlier today. Readers who are interested in more details should read the annual report itself.

- Insurance Underwriting. All of Berkshire’s insurance segments posted weaker underwriting results in 2019 compared to 2018, but in aggregate, insurance operations still produced a $325 million net underwriting profit which means that the cost of Berkshire’s $129 billion of policyholder “float” was still negative. GEICO posted a $1.5 billion pre-tax underwriting profit with a 95.8% combined ratio and Berkshire’s other primary insurers posted a $383 million pre-tax underwriting profit, also with a 95.8% combined ratio. However, Berkshire’s reinsurance operations posted a $1.5 billion pre-tax underwriting loss, mostly due to expected periodic underwriting losses from retroactive reinsurance contacts.

- Investment Income. Net investment income increased 21.4% to $5.5 billion in 2019 due to higher interest rates on short term investments and higher dividend income bolstered by Berkshire’s $10 billion investment in Occidental Petroleum 8% cumulative preferred stock.

- Railroad. BNSF posted net income of $5.5 billion in 2019, up 5% from 2018 despite a modest decline in revenue driven by a decrease in volume, partially offset by higher average revenue per railcar/units. An increase in revenues from industrial products was more than offset by declines in consumer products, agricultural products, and coal. The increase in net income was driven by a reduction in BNSF’s operating ratio (operating expenses/revenue) to 64.6% in 2019 compared to 66.9% in 2018. Berkshire acquired BNSF ten years ago for $26.5 billion.

- Utilities and Energy. Berkshire’s widely diversified portfolio of energy assets posted net income of $2.8 billion in 2019, up 8.3% from 2018. All of Berkshire’s utility operations posted higher pre-tax income in 2019. Somewhat counter-intuitively, Berkshire’s utility operations include the largest real estate brokerage in the United States which also posted higher profits in 2019. Buffett devotes part of his letter to discussing the twentieth anniversary of Berkshire’s initial acquisition of MidAmerican. Greg Abel, Berkshire’s Vice Chairman of non-insurance operations and potential successor to Buffett, came to the company via the MidAmerican acquisition in 2000.

- Manufacturing, Service, and Retailing. Berkshire’s building products group posted a 12.8% increase in pre-tax earnings on strength in the Clayton Homes operations which have been expanded in recent years from manufactured homes to more lucrative site-built homes. Industrial products had a 3.2% decline in pre-tax earnings driven by a large decline in Lubrizol’s results due to lost business associated with a fire at one of its facilities. Consumer products posted a 3.6% increase in pre-tax earnings driven by cost containment efforts at several subsidiaries and a new Duracell product launch, partially offset by lower RV sales at Forest River. Service group pre-tax earnings declined 8.4% compared to 2018 due to lower earnings from TTI and FlightSafety which was partially offset by higher earnings from NetJets. Retailing pre-tax earnings increased 1.6% compared to 2018 due to higher earnings at Berkshire’s automobile dealership operations partially offset by lower earnings at other retailing operations including the furniture group.

This is obviously a very abbreviated review of results, but there is little point in replicating the content contained within the annual report itself. Over twenty years of owning Berkshire Hathaway shares, the granularity of the reporting units has diminished significantly because smaller units, such as See’s Candies, that used to warrant specific disclosure are now too small to be material to overall results. The good news is that the report is still short enough to be read in a few hours.

Highlights from Warren Buffett’s Letter to Shareholders

Warren Buffett’s letters to shareholders are always fascinating to read and attract a great deal of attention. Although my view is obviously subjective, the letter seemed somewhat more abbreviated than usual, and in certain respects, was more somber.

Buffett opens the letter with a discussion of the power of retained earnings which was perhaps a response to an increasing amount of criticism regarding Berkshire’s ever growing cash balance. Over the past decade, Berkshire has invested over $121 billion internally in property, plant, and equipment, a fact that I validated from the cash flow data I’ve collected over the years. Buffett states that internal reinvestment in productive assets will “forever remain our top priority”.

Long-time students of Warren Buffett will recall that he used to discuss the concept of “look through” earnings frequently. The concept is straight forward: For Berkshire’s large portfolio of marketable equity securities, Berkshire records as income only the dividends that these companies pay. The majority of net income earned by these companies are retained. For Berkshire’s top ten holdings, retained earnings of the companies are more than double the dividends that are recorded as income by Berkshire:

Over time, assuming the retained earnings are reinvested well by these companies, Berkshire should benefit from appreciation in the shares. In the meantime, Buffett is obviously encouraging us to think about the entire scope of the economics of these businesses, not just the dividends that are paid to Berkshire.

In a subsequent discussion of Berkshire’s equity securities, Buffett has the following to say about fixed income securities:

“Forecasting interest rates has never been our game, and Charlie and I have no idea what rates will average over the next year, or ten or thirty years. Our perhaps jaundiced view is that the pundits who opine on these subjects reveal, by that very behavior, far more about themselves than they reveal about the future.

What we can say is that if something close to current rates should prevail over the coming decades and if corporate tax rates also remain near the low level businesses now enjoy, it is almost certain that equities will over time perform far better than long-term, fixed-rate debt instruments.”

Although he does not say so, it seems reasonable to infer that Buffett believes that rates will, at some point, adjust to a higher level. We can see this from the very low level of fixed maturity securities on Berkshire’s balance sheet relative to the overall portfolio.

Berkshire holds just $18.7 billion of fixed income securities of which 94% mature within five years. This is a tiny 4.6% of Berkshire’s $409 billion in cash and investments as of 12/31/19. Berkshire has not held less fixed income since 1997, prior to the General Re acquisition. In 1998, Berkshire held $21.3 billion of fixed income, or 28.5% of the company’s $74.6 billion in cash and investments as of 12/31/98!

Also, take a look at the interest rate risk section of the MD&A, a portion of which is shown below. Berkshire’s fixed income securities would produce a minimal loss for Berkshire even with a 300 basis point increase in rates. On the other hand, Berkshire’s debt would decline substantially in fair value should such an increase occur. In recent years, Buffett has taken advantage of low interest rates to issue debt at the parent company level as well as for BNSF and Berkshire Hathaway Energy. Any episode of higher inflation would allow this debt to be repaid with inflated dollars:

In a section named “The Road Ahead”, Buffett goes into some detail regarding the disposition of his estate which will occur over a lengthy period of time after his death. His Class A shares will be converted to Class B shares prior to being donated to foundations that will eventually sell the shares to fund initiatives. Buffett believes that market disruption from the sales will be minimal over the 12-15 year period following his death. Perhaps somber, but also reassuring to shareholders worried about large blocks of stock depressing the price.

2019 Repurchase Activity

Warren Buffett’s letter contains a brief section regarding repurchases noting that $5 billion was spent on buybacks in 2019 and inviting shareholders with $20 million or more that they would like to sell to contact the company directly, which could be seen as an aggressive move. However, he threw cold water on the idea that he’s super eager to buy back shares:

“Calculations of intrinsic value are far from precise. Consequently, neither of us feels any urgency to buy an estimated $1 of value for a very real 95 cents. In 2019, the Berkshire price/value equation was modestly favorable at times, and we spent $5 billion in repurchasing about 1% of the company.”

So, is Buffett saying that at current prices, Berkshire stock represents only a 5 percent discount to intrinsic value? That’s likely the conclusion many readers will come to, but let’s take a look at actual repurchase activity in 2019 to see if we can draw any conclusions from his actions:

Berkshire publishes the actual number of shares repurchased in each 10-Q and 10-K report which is where the data shown above was obtained. It reconciles to the $5,016 million figure presented in the statement of changes in shareholders’ equity on page K-69 of the annual report.

It may seem somewhat odd that more shares were not repurchased early in 2019 when the Class A shares traded near $300,000 and the Class B shares traded near $200. There was repurchase activity at that time, but it was relatively modest. The repurchase activity in November and December took place at higher prices. We can also infer that a modest number of shares have been repurchased this year based on the share count as of February 13, 2020 presented on the first page of the 10-K.

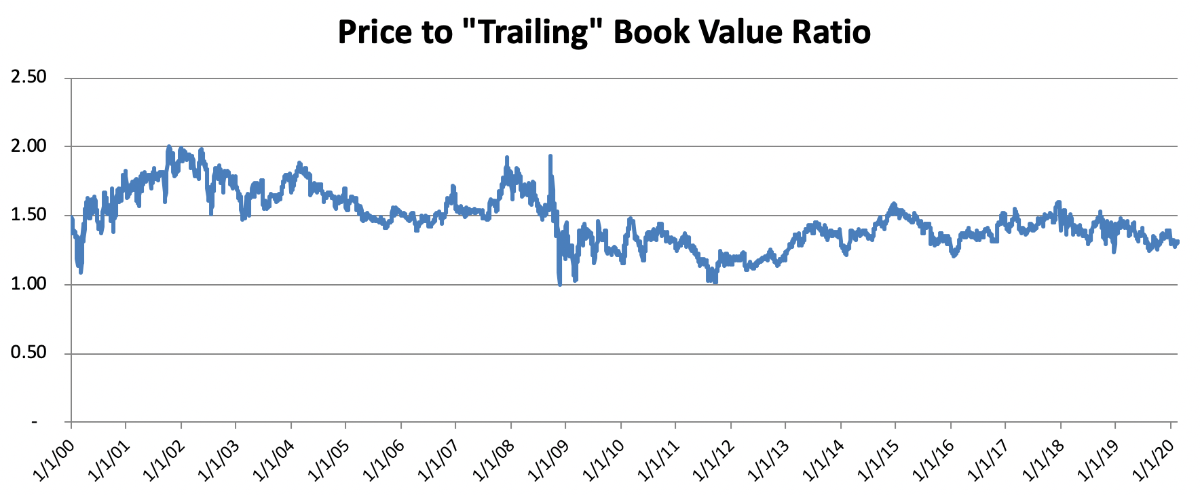

Of course, we should not look at the share price exclusively over time without understanding that intrinsic value also changes. Berkshire’s price-to-book ratio stands at 1.31 today compared to around 1.42 in late February 2019. This is because book value has increased significantly over the past year.

In his 2018 letter to shareholders, Buffett de-emphasized book value as a relevant benchmark for Berkshire, which I wrote about at the time. Still, it is worth noting that Berkshire’s price-to-book ratio is still quite modest relative to where it stood prior to the financial crisis, as seen in the graph below:

It seems reasonable to believe that Berkshire is quite interested in repurchasing large blocks of shares. Otherwise, there would have been no reason to invite large shareholders to contact the company directly should they wish to sell.

Questions for Ajit Jain and Greg Abel

For the first time, shareholders will be allowed to ask questions at the annual meeting specifically directed to Vice Chairmen Ajit Jain and Greg Abel. This move seems a bit overdue but is nonetheless welcome. I was one of several shareholders who asked for this change. Since it appears quite likely that either Abel or Jain will be the next CEO of Berkshire, it will be interesting to hear from them directly.

That’s all for this special Berkshire Hathaway issue of Rational Reflections. Please note that nothing in this newsletter is investment advice, about Berkshire specifically or any investment generally. While the data provided in this issue has been double checked, investors should read the filings directly and not rely on any facts or figures in this newsletter.

Any feedback is welcome and can be sent to administrator@rationalwalk.com. Thanks for subscribing!

Was this email forwarded to you by a friend or colleague? Sign up here to receive Rational Reflections directly every week.

Copyright and Disclosures

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.